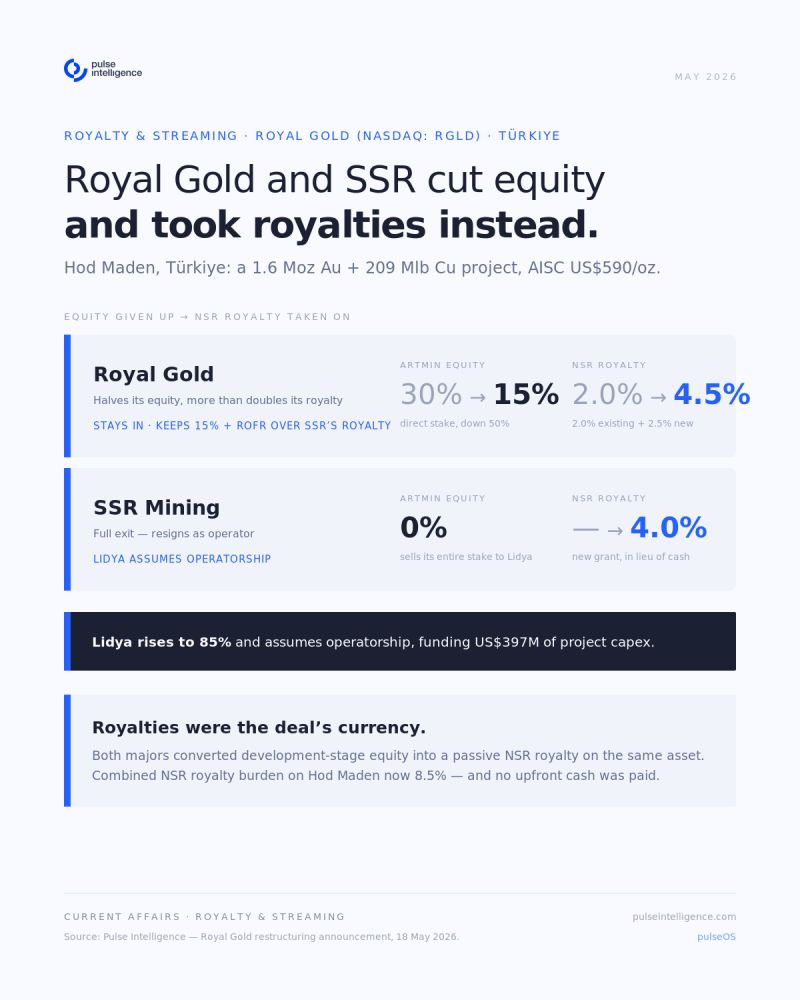

Royal Gold Inc. just cut its Hod Maden equity from 30% to 15%. SSR Mining Inc. exited entirely. Both walk away with new NSR royalties in lieu of their equity positions. No cash changed hands for the royalty grants; they came out of the restructuring itself.

The numbers worth circling:

Royal Gold: new 2.5% NSR layered on top of an existing 2.0%, creating a 4.5% effective royalty position, plus a residual 15% equity stake.

SSR Mining: new 4.0% NSR, full operational exit, Lidya Madencilik assumes operatorship and goes to 85% ownership.

Royal Gold also holds an option to acquire half of SSR's royalty (2.0% NSR) for US$160M, exercisable up to 12 months post-commercial production. On that basis, the implied value of SSR's full 4.0% NSR sits around US$320M.

The total private royalty burden on Hod Maden rises to 8.5%. At a by-product AISC of US$590/oz Au across a 13-year mine life carrying 1.6 Moz Au and 209 Mlb Cu, the project absorbs it.

Set this alongside the last 60 days of deal flow:

- Wheaton Precious Metals / BHP Antamina silver stream: US$4.3B (closed 1 Apr)

- Wheaton Precious Metals / KGL Resources Jervois Au-Ag stream: US$275M (1 Apr)

- OR Royalties / Sailfish Royalty (Spring Valley + Moonlight) NSR: US$168M (10 Apr)

- OR Royalties / Canadian Copper NB stream: US$28M (14 Apr)

The Wheaton-Antamina print is the headline number of 2026. But Hod Maden is structurally more interesting: a major royalty company converting development-stage equity into a passive cash-flow claim, and a producer using the same instrument to exit operatorship without crystallising a loss.

Same mechanism. Two different problems solved.

Worth watching which other JV-held development assets get this treatment next. Less searching. More strategising.™

Where does your team's data infrastructure sit today?

Answer 10 questions. Get a private diagnostic on your AI readiness — in minutes.

Less Searching. More Strategising.™

See the platform running on real mining data. Book a demo to see what this looks like for your team.