Zimbabwe suspended lithium concentrate exports. CATL's Jianxiawo mine stayed offline longer than expected. Beijing cancelled 27 mining permits across Jiangxi.

The result: lithium carbonate in China just touched its highest level in nearly three years, up around 50% since January.

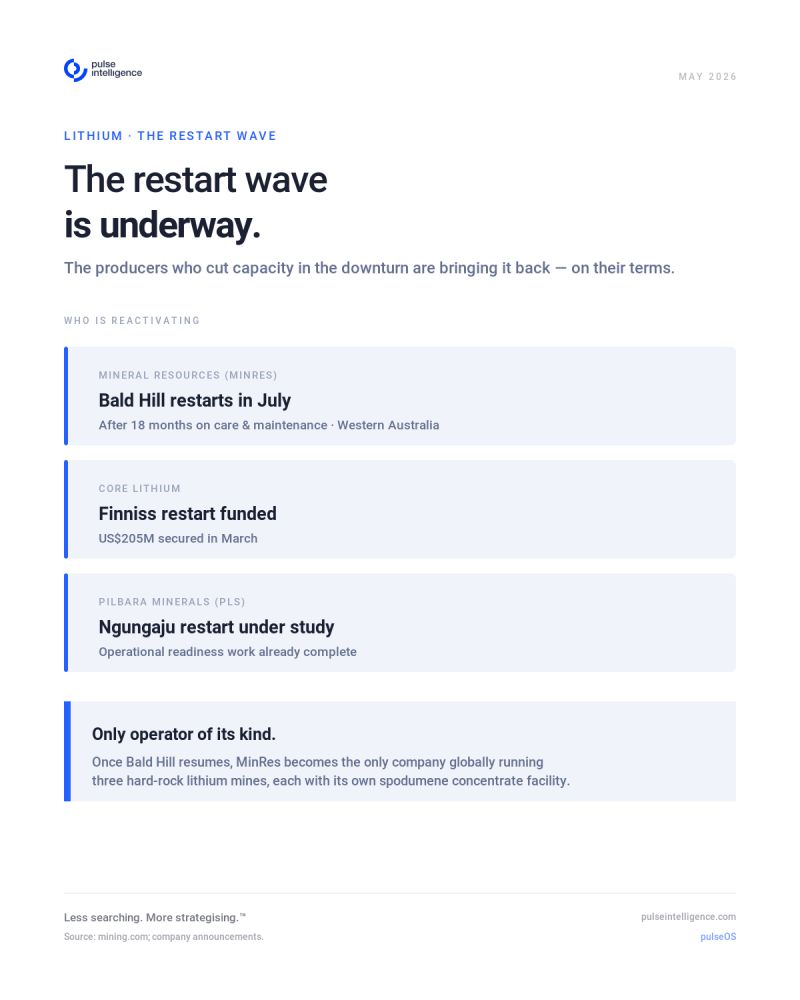

Now the restarts are coming.

Mineral Resources Limited announced that Bald Hill, its wholly owned lithium mine in Western Australia, will resume production in July after 18 months on care and maintenance.

Once operational, MinRes will be the only company in the world running three hard rock lithium mines with dedicated spodumene concentrate facilities.

And they are not the only ones moving.

Core Lithium locked in US$205 million to bring Finniss back online. PLS has been preparing a potential restart of Ngungaju, with operational readiness work already complete.

What is interesting here is not any single restart. It is the pattern.

Supply discipline during the trough created scarcity. Scarcity repriced the commodity. And now the same producers are reactivating capacity on their terms, not the market's.

For mining finance professionals tracking capital allocation across the battery metals chain, this is the cycle playing out in real time. The question is whether the supply response overshoots again, or whether the lessons of 2024 stick. Less searching. More strategising.™

Where does your team's data infrastructure sit today?

Answer 10 questions. Get a private diagnostic on your AI readiness — in minutes.

Less Searching. More Strategising.™

See the platform running on real mining data. Book a demo to see what this looks like for your team.