Hycroft Mining Holding Corporation just delivered a $10 billion after-tax NPV from its technical report.

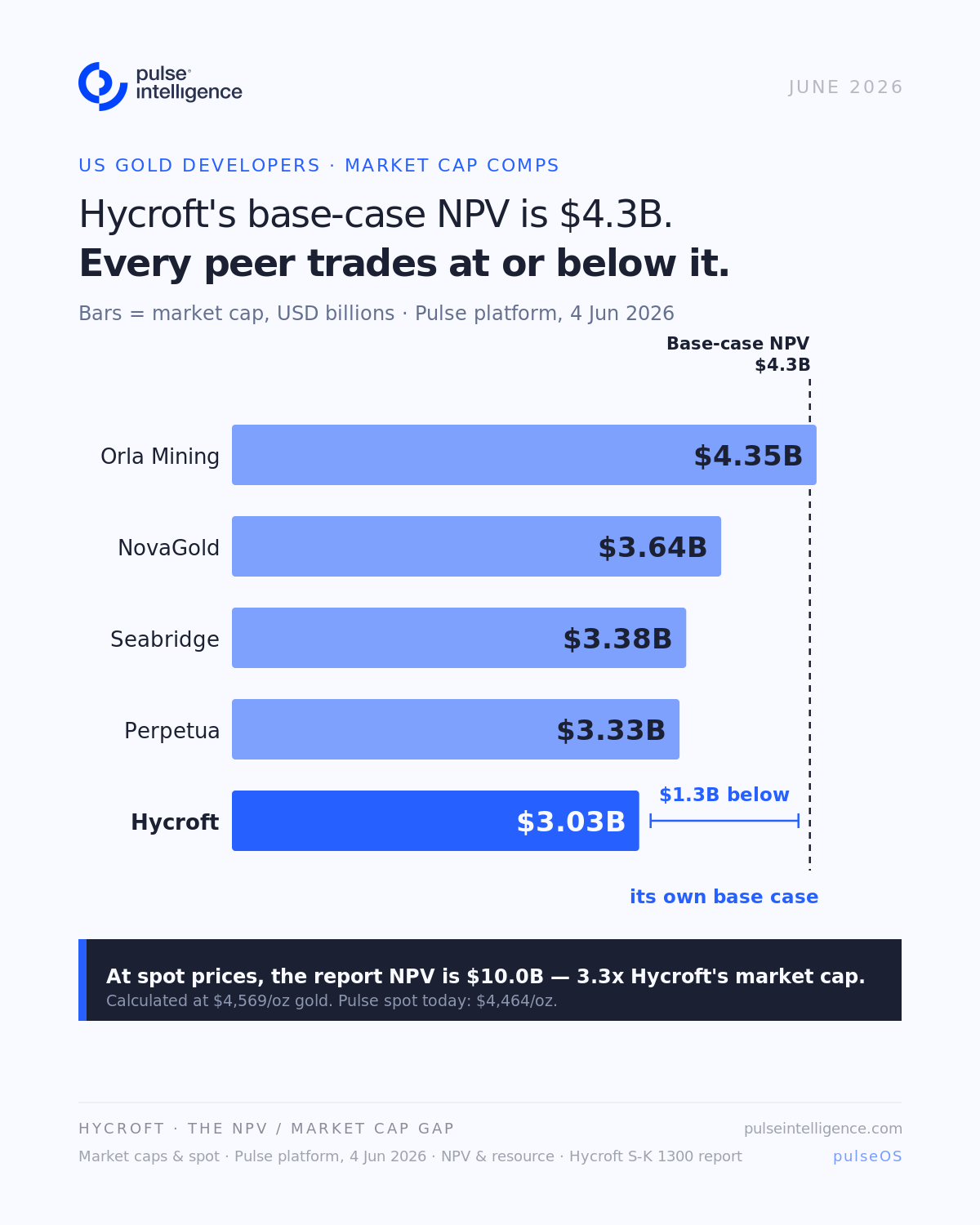

Its market cap is currently sitting around USD$3 billion.

That is a 3.3x discount to the stated spot-price value, in a Tier 1 jurisdiction, with a 51-year mine life and 30.1% IRR already attached.

To contextualise that gap, Pulse Intelligence pulled the comps across a few US gold development peers:

| Company | Market Cap |

|---|---|

| Orla Mining | $4.4B |

| NOVAGOLD | $3.6B |

| Seabridge Gold | $3.4B |

| Perpetua Resources | $3.3B |

| Hycroft Mining | $3.0B |

Every one of those peers is trading at or below Hycroft's base-case NPV of $4.3 billion, calculated at $3,600/oz gold and $48/oz silver. Gold is trading above $4,440/oz today.

The resource base is 16.4 million ounces of gold and 562.6 million ounces of silver in the M&I category. Infrastructure is already on site: crushing facilities, leach pad capacity, two Merrill Crowe plants. Initial capital: $2.4 billion.

Three things stand out analytically.

The silver optionality is underpriced. At $77.94/oz silver, the 562.6Moz endowment has a notional in-situ value above $43 billion, before processing costs or discounting.

The price leverage is extreme. Moving from base case to spot roughly doubled the NPV, from $4.3 billion to $10 billion. That sensitivity is a feature, not a flaw, for investors with a view on precious metals.

Only 15% of the 64,000-acre land position is covered by the current resource estimate. The exploration story has barely started. Less searching. More strategising.™

Where does your team's data infrastructure sit today?

Answer 10 questions. Get a private diagnostic on your AI readiness — in minutes.

Less Searching. More Strategising.™

See the platform running on real mining data. Book a demo to see what this looks like for your team.