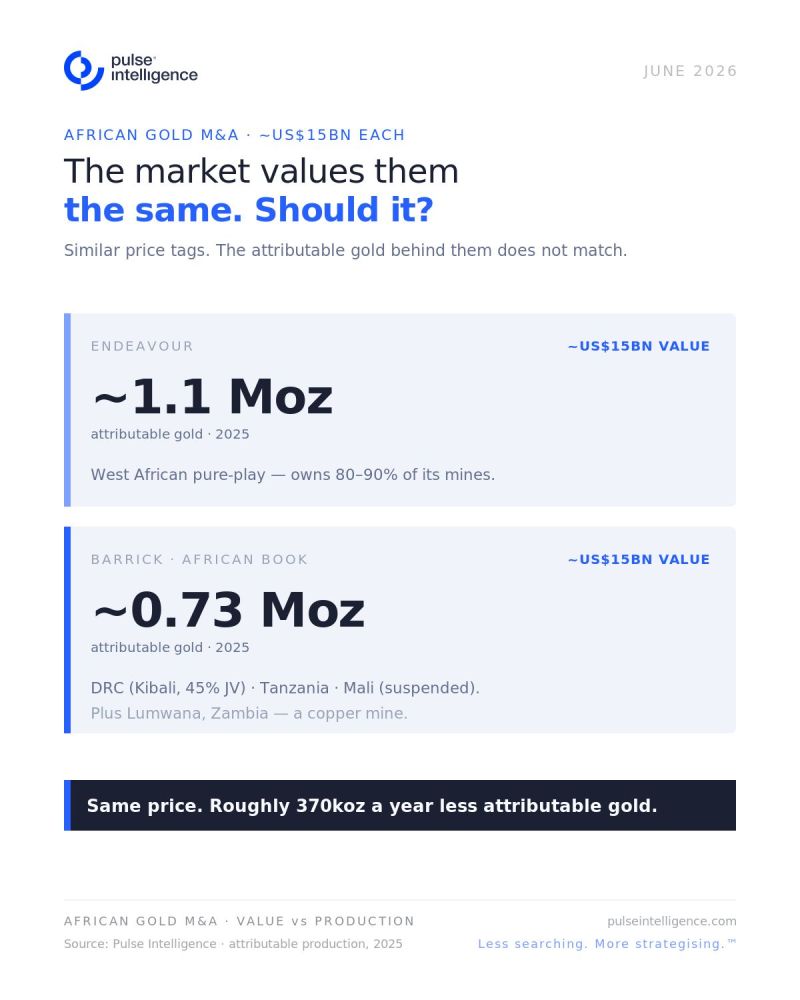

Barrick Mining Corporation and Endeavour Mining are reportedly each valued at around US$15 billion for this deal, and the market is calling it a merger of equals.

We ran both portfolios through Pulse Intelligence data to test whether that framing holds.

On production, the 100% comparison is close. Endeavour's five West African mines delivered 1.2 Moz in 2025 at an AISC of US$1,433/oz. Barrick's African gold assets, on a 100% operated basis, land at a comparable number.

Gold is currently US$4,479/oz. At that margin, every owned ounce matters more than every operated ounce.

Endeavour holds 80–90% of its mines. Barrick is different. Kibali in the DRC is a 45% JV. North Mara and Bulyanhulu in Tanzania are held at 84%, inside a mandatory gold-sale arrangement with the Bank of Tanzania. On an attributable basis, Barrick's Africa and Middle East segment produced 734,000 oz in 2025 — nearly 40% below the 100% figure.

There is a valuation gap the headline does not show. Endeavour's enterprise value is ~US$7.8 billion, against trailing EBITDA of ~US$2.7 billion, implying about 3.9x. Barrick trades at 6.4x group EBITDA. If the combined African entity reprices toward the peer average on a London listing, that gap is the deal's financial logic — and the number a market-cap comparison alone will never surface.

The structure tells the rest. Endeavour is a focused, high-ownership West African producer across Burkina Faso, Senegal, and Côte d'Ivoire. Barrick's African book spans the DRC, Tanzania, and Mali, where Loulo-Gounkoto sat suspended through most of 2025 in a dispute with the state. Lumwana in Zambia is a copper mine.

One press narrative worth scrutinising is Endeavour described as cautious about re-entering Mali. Kalana, a pre-feasibility development project there, has been in its portfolio since 2017 and remains today.

The broader Mali context sharpens that. Zijin Gold's C$5.5 billion all-cash acquisition of Allied Gold — including the Sadiola mine producing ~200,000 oz/year, with expansion to add 400,000+ oz/year — is delayed. Canadian and African regulators have cleared it. Beijing is deliberating. China's National Development and Reform Commission has flagged the 27% premium plus the political risks of Allied's Mali operations, pushing the outside date to 29 July 2026.

West Africa clearly carries a valuation gap from perceived political risk — a reason cited for Barrick to split its asset base entirely. After all, Barrick's Loulo-Gounkoto spent most of 2025 under state administration following gold seizures and the detention of senior staff.

Yet, as Randgold Resources proved years ago, and Endeavour is proving today, you can build a market-leading business in the region.

A combined Barrick/Endeavour entity with Loulo is an interesting valuation question. And it matters for how you price this. Less searching. More strategising.™

Where does your team's data infrastructure sit today?

Answer 10 questions. Get a private diagnostic on your AI readiness — in minutes.

Less Searching. More Strategising.™

See the platform running on real mining data. Book a demo to see what this looks like for your team.